A strip of water between Iran to the north and Oman and the United Arab Emirates to the south, the Strait of Hormuz has no particular grandeur. At its narrowest point, it is just 39 kilometres wide. And yet it is arguably the single most consequential chokepoint in the global economy, the place where a fifth of the world's oil and a significant share of its liquefied natural gas pass through on their way to markets across Asia, Europe and beyond. For decades, its closure was treated as a theoretical catastrophe, something Iran threatened and the world feared but never quite confronted. Since 28 February 2026, it has been confronting it.

The crisis began when the United States and Israel launched coordinated airstrikes on Iran under Operation 'Epic Fury', targeting military facilities, nuclear sites and leadership, and killing Supreme Leader Ali Khamenei. Iran's response was swift: retaliatory missile and drone strikes on US military bases, Israeli territory and Gulf states, and a declaration by the Islamic Revolutionary Guard Corps that the strait was closed. What followed has been described by the International Energy Agency as "the largest supply disruption in the history of the global oil market."

What the strait actually carries

To understand what its closure means, it helps to be precise about what normally passes through it. According to the US Energy Information Administration, around 20 million barrels per day of oil and petroleum liquids moved through the Strait of Hormuz in 2024, equivalent to about 20% of global petroleum liquids consumption. The IEA estimates that roughly 19% of global LNG trade also depends on Hormuz. The burden of disruption, however, falls unevenly. 84% of the crude oil and condensate moving through the strait in 2024 was destined for Asian markets. Japan alone receives about 70% of its Middle Eastern oil through Hormuz. China, India, South Korea and Taiwan are similarly exposed.

But the assumption that this is primarily an Asian problem misreads how global commodity markets work. Even where European dependence on Gulf crude is lower, disruption in Hormuz still affects diesel, freight, aviation fuel and inflation expectations through global pricing. Higher energy, fertiliser and transport costs may increase food prices and intensify cost-of-living pressures, particularly for the most vulnerable. The strait is also, as one analyst put it, an economic clock: a short closure is an oil shock, but a long closure becomes an inflation and growth shock.

The scale of the damage so far

Following the closure of the strait, Brent crude surged past $120 per barrel and QatarEnergy declared force majeure on all exports. The oil production of Kuwait, Iraq, Saudi Arabia and the UAE collectively dropped by a reported 6.7 million barrels per day by 10 March, and by at least 10 million barrels per day by 12 March. The Qatari LNG facility at Ras Laffan was struck by Iranian missiles, reducing the country's LNG export capacity by 17%, with repairs expected to take up to five years.

The maritime blockade triggered a concurrent food supply emergency across Gulf Cooperation Council states (GCC), which rely on the strait for over 80% of their caloric intake. By mid-March, 70% of the region's food imports were disrupted, forcing retailers to airlift staples, with consumer prices spiking between 40% and 120%. Iranian strikes on desalination plants deepened the crisis further: Kuwait and Qatar source 99% of their drinking water from desalination.

The ripples have spread far beyond the Gulf. In Europe, the conflict coincided with historically low gas storage levels, causing Dutch TTF gas benchmarks to nearly double to over €60 per megawatt-hour by mid-March. The European Central Bank postponed its planned interest rate reductions, raising its inflation forecast and cutting GDP growth projections, with economists warning that energy-intensive economies face high risks of technical recession if the maritime blockade persists through the summer refill season. The Federal Reserve Bank of Dallas estimates that the Hormuz closure could lower global real GDP growth by an annualised 2.9 percentage points in the second quarter of 2026.

Why there is no real alternative

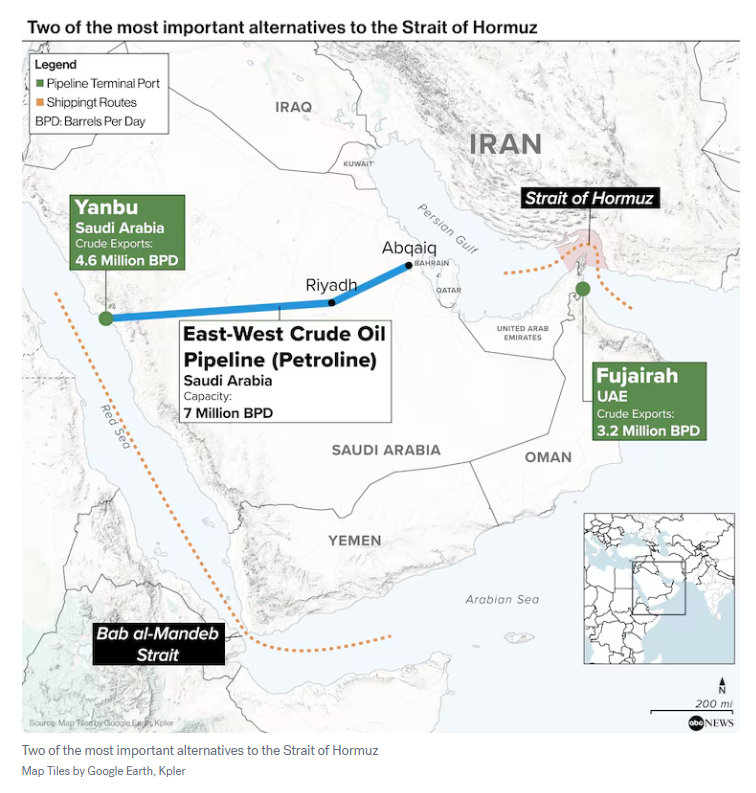

When the crisis began, much attention turned to alternative routes. The reality, examined closely, is sobering. Three pipelines exist as potential bypasses. Saudi Arabia's East-West Pipeline runs 1,200 kilometres from Abqaiq to the Red Sea port of Yanbu. The UAE's Abu Dhabi Crude Oil Pipeline connects the Habshan field to the port of Fujairah. Iraq's Kirkuk-Ceyhan pipeline reaches the Mediterranean via Turkey, though Iraq's southern fields, which produce the bulk of its exportable crude, have no meaningful inland connection to it.

The problem is capacity and vulnerability. The IEA estimates that only 3.5 to 5.5 million barrels per day can be redirected through Saudi and Emirati pipelines. Against a baseline of 20 million barrels per day, the implied net shortfall is roughly 14.5 to 16.5 million barrels per day. And even the pipelines that exist are not safe. They are land-based and within range of Iranian missiles and drones, making them high-value, static targets. Drone attacks on the UAE's Fujairah port in March disrupted loadings at the Abu Dhabi pipeline terminus. For liquefied natural gas there are effectively no alternative export routes outside the strait at all.

Shipping rerouting offers partial relief at significant cost. The main maritime alternative is sending tankers around the Cape of Good Hope, which adds substantial time and cost, and only helps oil not already trapped in the Persian Gulf. Container vessels have been redirected to ports outside the strait, notably Fujairah and Khor Fakkan in the UAE and Oman's Sohar, with cargoes then moved by truck to their destinations. But Omani alternative ports including Duqm and Salalah have themselves come under drone attack, and the Joint War Committee of the London insurance market has placed waters around Oman on its list of high-risk maritime areas.

Ships avoiding Hormuz and the Suez Canal are being pushed onto longer routes around the Cape of Good Hope, creating new security risks as congested and poorly patrolled routes attract piracy, which is on the rise again off the Somali coast. The Red Sea, the other natural alternative, offers no comfort either: the Houthis have threatened to resume attacks on shipping there in support of the Iranian regime, putting the Yanbu pipeline route at risk too.

The conclusion drawn by energy analysts is stark. Beyond the limited pipeline options, there is no equitable backup plan to the Strait of Hormuz. The world built its energy architecture around a single chokepoint and has spent decades hoping no one would actually use it.

Iran's strategy: the soft closure

Iran has not declared a total blockade in the legal sense. Shipowners face congestion, repeated demands to identify themselves, electronic interference, drone and missile risks and uncertain insurance conditions. In practice, a soft closure can inflict much of the same damage as a declared blockade: if the risk is high enough, ships stop sailing.

The comparison with the Iran-Iraq Tanker War of the 1980s is instructive. During that conflict, hundreds of ships were struck, yet passage through the strait never came to a halt. Today, attacks are having a much larger impact on oil markets with far less hostile action. The difference lies in the globalised, just-in-time nature of energy and supply chains, and in the instant repricing of insurance risk.

Iran's anti-ship cruise missile arsenal further complicates any military solution. It includes short-range systems with 35-kilometre ranges, mid-range Noor-class missiles capable of striking at 120 to 300 kilometres, and the Soumar and Paveh cruise missiles with ranges up to 1,000 kilometres. These can be fired from deep inland, significantly enhancing the survivability of their launchers against US and Israeli airstrikes. Iran, in other words, does not need to control the strait militarily to make it commercially unusable.

Iran has also used selective exemptions as a diplomatic tool, permitting ships from countries it considers friendly, among them China, Russia, India, Iraq, Pakistan, Malaysia and the Philippines, to transit under bilateral arrangements. Iraq was declared exempt from restrictions, a move with the potential to release up to three million barrels a day of Iraqi crude, though an Iraqi official cautioned that the usefulness of the exemption depends entirely on whether shipping companies are willing to risk entering the strait at all. Some ships, according to reports, have paid up to $2 million to use an Iranian-controlled channel north of Larak Island.

The international response and its limits

The IMO convened an Extraordinary Session of its Council in March to examine the impact on international shipping and seafarers, with Secretary-General Arsenio Dominguez stating that seafarers must not be targets, and that the situation was unacceptable and unsustainable. On 27 March, UN Secretary-General António Guterres announced the establishment of a dedicated Task Force, including IMO, UNCTAD and the International Chamber of Commerce, to develop technical mechanisms to address humanitarian needs in the strait. On 2 April, Dominguez told ministers from more than 40 countries that fragmented responses were no longer sufficient.

Around 20,000 civilian seafarers remain aboard vessels unable to transit the strait, facing dwindling supplies, fatigue and severe psychological stress, with 10 seafarers confirmed killed since hostilities began. Some 2,000 ships are stranded in the region amid Iran's partial blockade.

On the diplomatic front, the UN Security Council remains gridlocked. A Bahrain-led proposal was postponed on 4 April amid divisions among major powers: Russia and China have been concerned that any resolution could justify military action near Iran and risk escalation. On 5 April, France and South Korea announced they would work jointly toward reopening the strait. Zelensky offered Ukraine's expertise in creating safe maritime corridors, drawing on its experience keeping Black Sea ports open despite Russian attacks.

OPEC+ met on Sunday and agreed to raise output quotas by 206,000 barrels per day for May, the same modest increase agreed in March. Analysts described the move as largely symbolic as the same war disrupting global oil flows is preventing most producers from actually pumping more. Only Saudi Arabia and the UAE hold meaningful spare capacity, and both face the same export bottleneck through the Gulf. The 206,000 barrel increase represents less than 2% of the supply disrupted by the closure of the strait.

The ceasefire proposal and Tuesday's deadline

As of Monday 6 April, a two-phase peace proposal brokered through Pakistan is on the table. It envisions an immediate ceasefire followed by a comprehensive agreement within 15 to 20 days, with Pakistan's army chief maintaining overnight contact between Washington and Tehran. Iran has confirmed receiving the proposal, but a senior Iranian official told Reuters that Tehran will not accept deadlines, will not reopen the strait as part of a temporary arrangement, and sees Washington as unprepared for a permanent ceasefire.

Trump, for his part, issued an ultimatum on Sunday, threatening to strike Iranian power plants and bridges if the strait is not open by 8pm Eastern Time on Tuesday. Fresh strikes were reported across the region on Monday. The IRGC, meanwhile, announced it was finalising what it called a new order for the Persian Gulf, warning that conditions in the strait would never return to what they were before the war.

Shipping and trade experts warn that even if the waterway were to reopen immediately, the disruption to global supply chains would be felt for months, as hundreds of vessels race simultaneously to call at Persian Gulf ports, creating a backlog the system is not equipped to absorb quickly. Hapag-Lloyd's communications chief Nils Haupt put it plainly: when the war is officially over, the real work starts. The logistics war outlasts the military one.

Sources: Reuters, Al Jazeera, CNBC, IMO, Maritime Security Forecast, Chatham House