When KPMG delivered a business plan to the Natural Gas Infrastructure Company (ETYFA) in November 2024 for the liquefied natural gas (LNG) reception terminal development project at Vasiliko, the government had literally everything at its disposal to "lock in" the project's restart after the Chinese consortium's withdrawal: a situational assessment, a comprehensive risk analysis, implementation timelines with alternative scenarios (accelerated, baseline, extended), and specific options for tendering strategy - from separate EPC/FSRU/OM contracts to a unified BOM (Build-Operate-Maintain) model with a single contractor.

In spite of this potentially positive outlook, in the following months no decisions were reached on a series of necessary actions: the critical tenders (Project Manager, new Owner's Engineer, infrastructure completion, LNG procurement) did not proceed, no binding roadmap was developed, and the construction site remains closed. This inertia had a direct impact on the project's cost, which was burdened by the withdrawal of European funding.

The study that Politis discloses today, clearly indicates that the revoking of funding by the European Commission was not really a lightning strike which the government could not have known about, as its disbursement was also dependent on work progress.

In other words, even if there had been no problems with the project's award, the grant would still have been lost due to lack of tangible progress! By the end of 2024 there should have been certification of project completion, a deadline that had come and gone.

What wasn't done

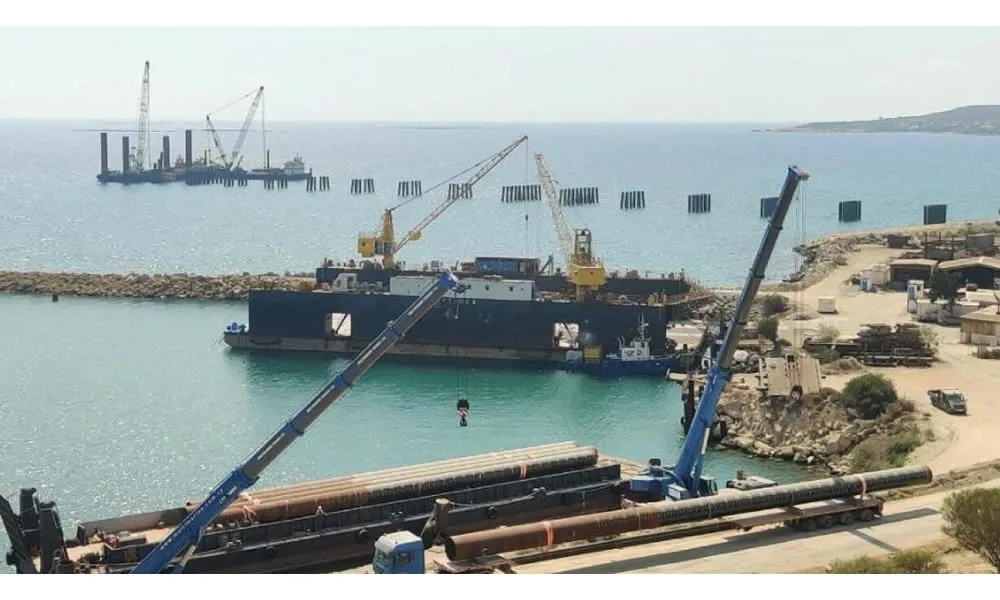

The KPMG study, which Politis gained access to, was detailed and precise about how the project's restart could be accomplished. After the contract's termination (July 2024), ETYFA took over the Vasiliko site, with parts of the project incomplete or exposed to decay and with an estimated remaining completion cost of €136.5 million (FSRU floating unit approximately €10 million, jetty/mooring dock approximately €68.5 million, onshore works approximately €57.5 million).

The possibility of compressing time could only have been achieved with a corresponding cost premium and strong administrative capacity during the work, since multiple parallel tenders required adequate, experienced personnel and decisive management. All this in November 2024.

On the financial side, KPMG warned that the financing gap would be the central obstacle. The overall structure was based on European grant funding (initially €101.2 million, readjusted to €99.8 million), EIB/EBRD loans (€150+80 million) and the EAC's own capital (€43 million), with most already received and an available grant balance of approximately €24.1 million under strict conditions.

The estimate of additional completion needs along with operational and legal pending issues gave a baseline gap scenario of approximately €179 million that would need to be covered primarily through state support, with a large range of variation depending on the outcome of the London arbitration (positive outcome: reduction via €67.5 million compensation; negative: surge with claim up to €184.5 million). The study itself noted that time, legal uncertainty, and regulatory pending matters (WACC, RAB) multiplied the risk.

The European grant

The most sensitive point was the European funding from CINEA (European Climate, Infrastructure and Environment Executive Agency), as there were two conditions for disbursement of the balance:

a) Adequate recognition of eligible expenditures up to 2023. The initial commitment was €101.2 million, which was readjusted to €99.8 million because recognized costs by the end of 2023 reached 98.6% of the target, resulting in a proportional reduction of the maximum eligible grant.

b) Certified completion by December 2024. As this particular deadline also passed without completion, the balance became practically impossible to collect without an extension. Simultaneously, the European side escalated legal contestation, in the shadow of the European Public Prosecutor's Office (EPPO) investigation into the award/execution procedures.

The result, after failing to utilise the window for securing an extension and concrete progress, was the EU decision to cancel/recover the grant: Cyprus is called to return €67.2 million it received until November 6, 2025, with interest in case of non-timely payment.

The cancellation of the European grant widens the financing gap. In the "soft" negative scenario where CINEA's recovery does not also trigger termination (cross-default) of the EIB/EBRD loans, the additional burden is immediate and financially painful, increasing the state burden and jeopardising project continuation without alternative sources.

In the "hard" scenario where the European grant cancellation triggers the right of immediate loan repayment, amounting to €217 million, the hole shoots up to a scale threatening viability - KPMG considered that as low probability due to state guarantees, but not impossible, especially if trust relations with institutional lenders deteriorate.

In any case, the need for new capital becomes greater, more expensive, and significantly more difficult.

Political ineptitude also had an operational impact. The work is deadlocked, but bills are still running. Safe-keeping, insurance, FSRU technical services of temporary support and delivery, the legal cost of arbitration. It’s leaking money everywhere, but commercial operation wise, it is not any closer than it was.

Publicly, the government continues to throw its weight behind the work, insisting it will be ‘concluded’, while at intervals, new technical advisors are brought in for assessments and gap analysis. All that aside however, as repeatedly reaffirmed in parliament debates, there is nothing tangible. No binding timeframe, no political decisions on which of the strategic implementation options to follow, a weakness which undermines every negotiation seeking extensions or support from European and international banking institutions.

In the meantime, the country remains without natural gas. On a day to day basis, this essentially means more expensive electricity production, delays in environmental targets and constant exposure to the cost of missing European directives on gas emissions. It is all passed on to households and businesses every month.

If the work had progressed on time, based on the ‘fast-track’ scenario, the estimate referred to completion by the end of this year, early 2026 at the latest. Instead, we have a different outcome. The European subsidy is gone, the funding is blowing up into a hole and the result of the arbitration is yet another known, potentially costly factor carved into the equation, leaving the budget of this work much as it is now. No funding roof to call home.